THB #253: Disney Q4 Results

Undeniably unimpressive.

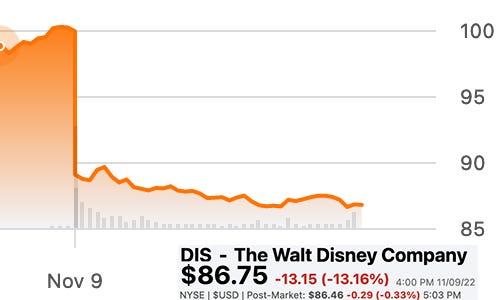

But the drama!!!

Investors on Wall Street are obviously smart. But it is amazing how stupid they can be sometimes. They are like comic book characters, set off in a positive or negative direction by the slightest of things, throwing aside all fundamentals on a mood… a whim.

As anyone who reads this newsletter on the regular knows, I think Bob Chapek has made some terrible choices. But nothing fundemental changed about Disney this week.

Bob Chapek told the world that streaming would not be profitable in 2022 or 2023… but somehow this is a major disappointment.

For years, as people screamed for the legacy media companies to switch to streaming faster… FASTER!… I wrote about what was obvious then and remains obvious… the revenues from legacy media platforms were bigger than streaming revenues will be anytime in the next 30 years. That is why they ALL dragged their feet.

Yes, the legacy companies can behave like Luddites. But you have to put a gun to the head of an i…

Keep reading with a 7-day free trial

Subscribe to The Hot Button by David Poland to keep reading this post and get 7 days of free access to the full post archives.